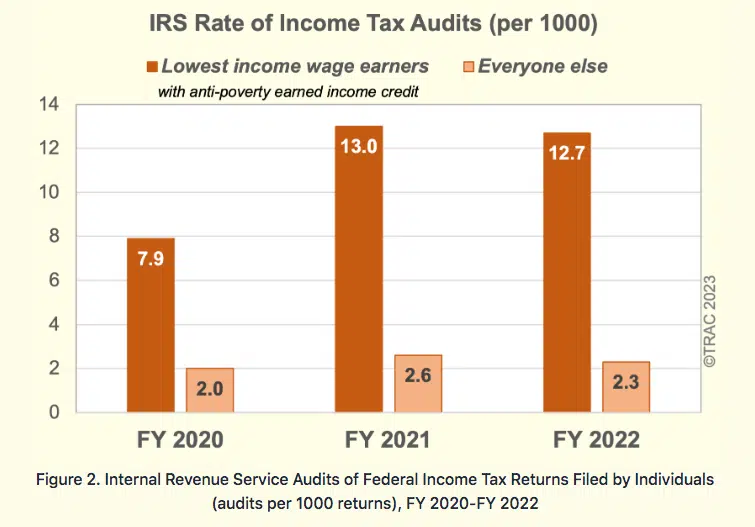

A new investigation by the International Consortium of Investigative Journalists (ICIJ) has revealed concerning disparities in how the Internal Revenue Service (IRS) conducts audits among taxpayers. The report suggests that the agency’s practices disproportionately target small businesses and self-employed individuals while taking a softer approach with large corporations and ultra-wealthy taxpayers.

Small Business Owners and Self-Employed Individuals Get More Criminal Referrals

One of the most striking findings highlighted in the ICIJ report is the vast difference in criminal referrals made by different IRS divisions. According to newly obtained data, over the past five years.

The Large Business and International Division (LB&I), which oversees audits of large corporations and ultra-wealthy individuals, flagged no more than 22 instances of possible tax crimes for further investigation.

In contrast, the Small Business and Self-Employed Division referred 848 cases that showed merits to open a criminal investigation during the same period.

Also read: TurboTax Kept the Government from Developing Free Tax Filing Software for Decades

This disparity exists despite the fact that LB&I oversees trillions of dollars in annual income from some of the nation’s largest taxpayers. The data has raised concerns among some current and former IRS officials about whether the agency is adequately pursuing potential criminal tax evasion by powerful corporate and individual taxpayers.

“I was putting butchers, bakers and candlestick makers in jail, but the big stuff we really wanted to go after was being ignored,” said Michael Welu, a former IRS agent who worked across multiple divisions during his 30-year career at the agency.

Cultural and Procedural Differences May Tip the Scale in Favor of the Rich

The ICIJ investigation points to several factors that may contribute to the LB&I’s softer approach:

- Different Audit Rules: LB&I is bound to follow a different set of audit procedures that provide large corporate taxpayers with more information and opportunities to influence the process. For example, LB&I auditors must share their audit plans with taxpayers in advance and allow them to suggest changes.

- Reluctance to Use Legal Tools: Current and former agents report that LB&I is often hesitant to use legal tools like summonses to obtain critical information from uncooperative taxpayers. One anonymous LB&I agent told ICIJ that when he asked colleagues about how to issue a summon, he was told that “no one was familiar with it.”

- Management Culture: Some agents describe an office culture where managers discourage the aggressive pursuit of large cases and are quick to dismiss suggestions of criminal behavior by wealthy taxpayers.

- Resource Constraints: Years of budget cuts have left the IRS struggling to match the legal and accounting firepower of large corporations and wealthy individuals.

- “Revolving Door” Concerns: The movement of personnel between the IRS and major accounting/law firms has raised questions about potential conflicts of interest.

Nina Olson, who served as the IRS National Taxpayer Advocate for 18 years, described LB&I’s approach as a “bespoke audit process” that provides additional protections to large corporations and wealthy individuals.

Also read: The IRS Won’t Arrest You For Not Reporting $10K+ Crypto Transactions… Yet

“With LB&I, you get a custom-made suit. With the Small Business and Self-Employed Division, you get it off the rack whether it fits you or not,” Olson told the ICIJ.

Impact on Tax Collection is Significant

How the two departments mentioned earlier enforce the country’s tax laws is having a massive impact on the so-called “tax gap”, which is the difference between what the agency should be collecting and what is owed.

According to data from the Treasury Department, the IRS’s parent branch, America’s top 1% is responsible for no less than 28% of that gap. This would amount to over $160 billion in unpaid taxes that the agency fails to collect every year. You would think that the IRS would focus most of its time and resources on closing that massive gap but that doesn’t seem like its focus.

Some current and former IRS agents worry that the LB&I’s enforcement style encourages continued non-compliance by wealthy taxpayers who know that they are unlikely to face criminal consequences. “Normal taxpayers are scared of the IRS — they fear real consequences,” one anonymous LB&I agent told ICIJ. “These highly wealthy people, it’s more like a game to them.”

The low number of criminal referrals from LB&I has frustrated officials in the IRS Criminal Investigation Division. Don Fort, who led the division until 2020, called LB&I’s referral numbers “ridiculous” and described its inner workings as “an ingrained culture where they don’t like to serve summonses, they don’t like to do fraud referrals.”

Case Study: An Investigation Into Caterpillar That Was Abruptly and Unexpectedly Stopped

The ICIJ report points to the 2017 investigation into the manufacturing giant Caterpillar as an example of the challenges in pursuing criminal cases against large corporations. Federal agents, including IRS criminal investigators, raided three Caterpillar facilities as part of a probe into the company’s offshore tax practices.

However, according to two seasoned IRS agents who are familiar with the case, LB&I only referred Caterpillar to criminal investigators after the Criminal Investigation Division had already opened its own inquiry. “It’s Caterpillar — LB&I had been auditing them forever. How could they have missed these issues?” a supervisory agent within the Criminal Investigation Division told ICIJ.

The Caterpillar investigation was abruptly halted in 2018 under circumstances that are now being investigated by two US senators for possible political interference.

IRS Response and Justification

In response to the ICIJ’s findings, the IRS defended the practices of its department. The agency emphasized that the cases handled by this unit are quite complex as they involve large multinational corporations. IRS spokesperson Robyn Walker stated that “these internal controls and checks and balances generally limit the opportunity for criminal activity” among large corporations.

Also read: Understanding IRS Federal Mileage Rates for 2023 and 2024

The agency also pointed to differences in the nature of potential non-compliance between large corporations and smaller businesses. “Instead, noncompliance for this population often presents itself in the form of disputes between the IRS and the taxpayers as to whether a taxpayer’s position is consistent with laws and regulations,” Walker explained.

Concerns About the “Revolving Door”

The ICIJ investigation raised questions about the movement of personnel between the IRS and firms in the private sector that represent large taxpayers. A review of LB&I executive lists covering the past 13 years found that out of 114 top executives named, at least a quarter had either worked for a major accounting firm, tax consulting firm, or major tax law firm shortly before joining the IRS or left the IRS to go to one of these firms.

This “revolving door” has drawn criticism from some lawmakers and watchdog groups. Senator Elizabeth Warren told ICIJ: “It undermines trust in government and our tax system when IRS employees go back and forth between government service and lucrative jobs with big accounting firms and other giant corporations.” The IRS is far from the only government body with a revolving door problem in the US, but it’s problematic nonetheless.

The IRS defended its hiring practices, stating that it needs private sector talent to tackle complex tax issues. The agency said that it has “a strong system of checks and balances in place to ensure fairness in its compliance activities,” including review processes to shield decisions from outside influences.

Biden Administration’s Efforts to Address Wealth Inequality

President Joe Biden’s administration has been intentionally addressing the issue of inequality in the tax system and they have pushed reforms designed to pressure wealthy individuals and large corporations to pay their “fair share”.

Two years ago, Biden managed to get Congress to approve $80 billion to bolster the IRS for the next decade. The administration said that the funds would be used to modernize the agency’s technological infrastructure and improve its customer service. However, some are worrying that this money will only be used to go after more small business owners and self-employed people (and, judging by the ICIJ report, they have good reason to).

However, Treasury Secretary Janet Yellen has reportedly directed the IRS to focus this new enforcement funding on taxpayers with incomes above $400,000, explicitly stating that audit rates for those earning less than $400,000 annually should not rise above historical levels.

In addition, these new resources should help the agency strengthen its enforcement actions and help it invigorate its practices to tax novel assets like cryptocurrencies.

Political Opposition and Talent Retention Make Things Difficult to the IRS

Despite this injection of funds, some long-standing issues are still affecting the IRS’s ability to improve its tax collection processes on the richest cohorts of society.

The ICIJ report highlights that a cultural change needs to occur within the government agency to ensure that outdated practices that swept things under the rug for wealthy taxpayers no longer prevail.

Also read: Controversial New IRS Crypto Reporting Rule is “Impossible to Follow”

Moreover, they highlight that government salaries are often not enough to retain top talent and that the best agents are continually recruited by big accounting firms with which the IRS just can’t compete in terms of compensation and benefits.

Finally, certain political factions have opposed the measures proposed by the Biden administration and the ongoing overhaul of the IRS, possibly as it affects key donors.

This latest report from the ICIJ has shed light on the disparities that occur within the IRS in terms of how it approaches different categories of taxpayers and how audits are conducted.

The current administration has been pushing efforts to equalize how taxpayers are treated but the IRS has already acknowledged that the complexity of auditing large corporations and wealthy individuals creates a natural gap that they don’t have the resources to fully close.

As the agency works to implement changes to its culture and procedures by using this new funding, it faces the challenge of not only increasing its enforcement capabilities but also addressing internal practices that may be undermining its ability to ensure fair and equitable tax compliance across all taxpayer groups.